Selling Property? Ways To Minimise Long-Term Capital Gains Tax

Among the several costs that you incur when you sell your home or other assets is the capital gains tax. Makaan IQ explains how you can minimise the tax amount by going for the right calculation method.

What is capital gains tax?

When you sell assets such as stocks, bonds, bullion and real estate, you are supposed to pay taxes — short-term and long-term — on the profit margin. This is known as the capital gains tax. For capital gains to be considered long-term, the period is three years for real estate assets and one year for equities. A seller also has to pay long-term capital gains tax on the property attained as a gift or in inheritance. In such cases, the cost of acquisition of property will be considered to be the price at which the previous owner bought the property.

In case the sales proceed are not invested in the options prescribed under Section 54 of the Income Tax (I-T) Act, the profit would be taxed either at 10 per cent without indexation or at 20 per cent, if indexation is applied. (Indexation is the process that takes into account the inflation in prices from the time a property is purchased till the time it is sold.) There is also a restriction that the sale proceeds of one property cannot be utilised for buying more than one property within India to avail of the benefit.

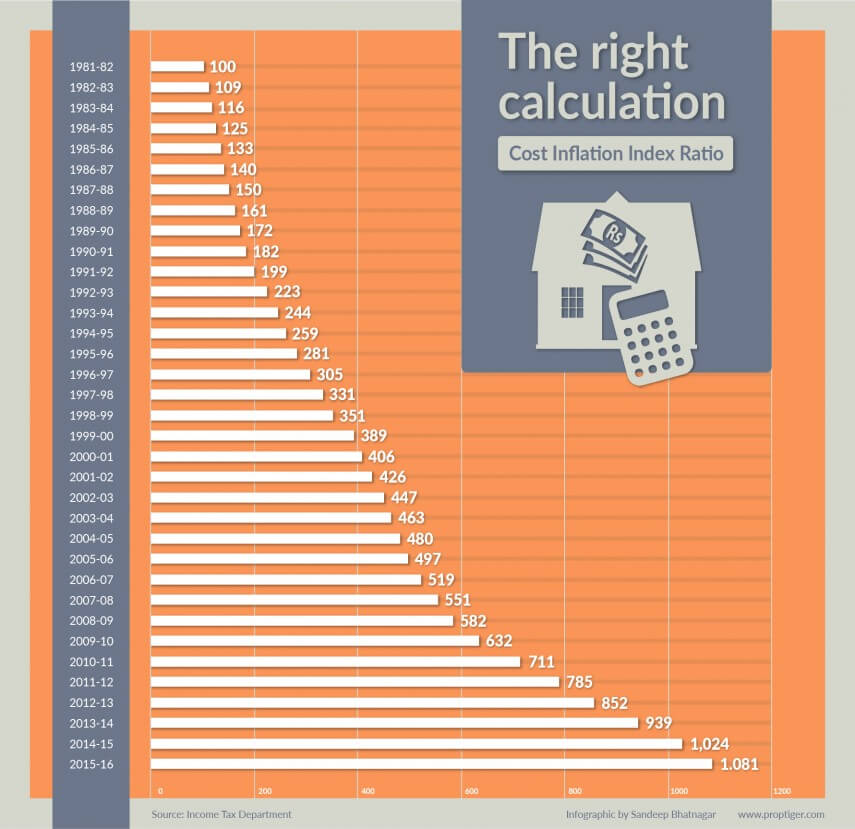

Calculating the liability

There are two methods to calculate the tax liability on long-term capital gains:

Method 1

Suresh Kumar bought a flat at Rs 10 lakh and after retaining it for three years, he sold it for Rs 15 lakh. Kumar earned Rs 5 lakh as profit in the process. According to government norms, he has to pay 10 per cent on the profit (Rs 50,000) as long-term capital gains tax.

Method 2

Another way to calculate you tax liability is to keep into account the indexation ratio. Going by the same example, Kumar, who bought the aforesaid property in financial year 2012-2013 and sold it in FY15-16, can arrive at the indexed cost of acquisition by dividing the ratio of the Cost Inflation Index (CII) of 2015-16 with the ratio of 2012-13. The sum then has to be multiplied with the original acquisition value.

Taking into account the government indexation, the value of the Rs 10-lakh house would now be Rs 12.68 lakh (1,081/852). Now, we can subtract the indexed cost of acquisition from the sale price of the property. Subtracting Rs 12.68 from Rs 15 lakh, we get Rs 2.32 lakh. We now have to apply the capital gains tax at 20 per cent, which would loosely translate into Rs 46,250.

Therefore by choosing method 2, a saving of Rs 3,750 can be made hence minimising the tax outgo. So a judicial selection between the two available methods needs to be done.

Exemptions available under Long-Term Capital Gains Tax

Section 54 of the I-T Act, 1961, lays out the various exemptions available under long-term capital gains from property.

- The proceeds from the sale of a residential house could be used to buy another residential house. However, this purchase has to be made within India and only a single residential house can be bought. The property can be bought either one year before or two years after the transfer of your property. In case property construction, it can be within three years from the date of transfer.

- Investment in bonds specified under Section 54EC can also be utilised to save taxes. By investing in government bonds such as the National Highways Authority of India and the Rural Electrification Corporation, etc., you can save on taxes. These bonds have to be purchased within six months from the date of transfer of property. These bonds come with a lock-in period of three years. The amount invested in such bonds cannot exceed Rs 50 lakh in one financial year.

- The money can be made tax-free by depositing it with a nationalised bank under the Capital Gains Account Scheme. Thereafter, the amount can be withdrawn only towards the purchase or construction of a house. The amount has to be used within three years. But if the amount remains unused after the expiry of the three-year-period, it would be liable to be charged under the long-term capital gains.